41% of Americans Expect the Housing Market to Crash in the Next Year, With the Majority Blaming Inflation

Rising inflation, high credit card debt and mass layoffs have many Americans concerned they’re in a recession. With the economy so uncertain, many wonder: Will the housing market crash, too? As it turns out, just over 2 in 5 (41%) consumers think it will in the next year, according to the latest LendingTree survey of more than 2,000 Americans.

This survey asked consumers about their housing market fears — here’s what else we found.

Key findings

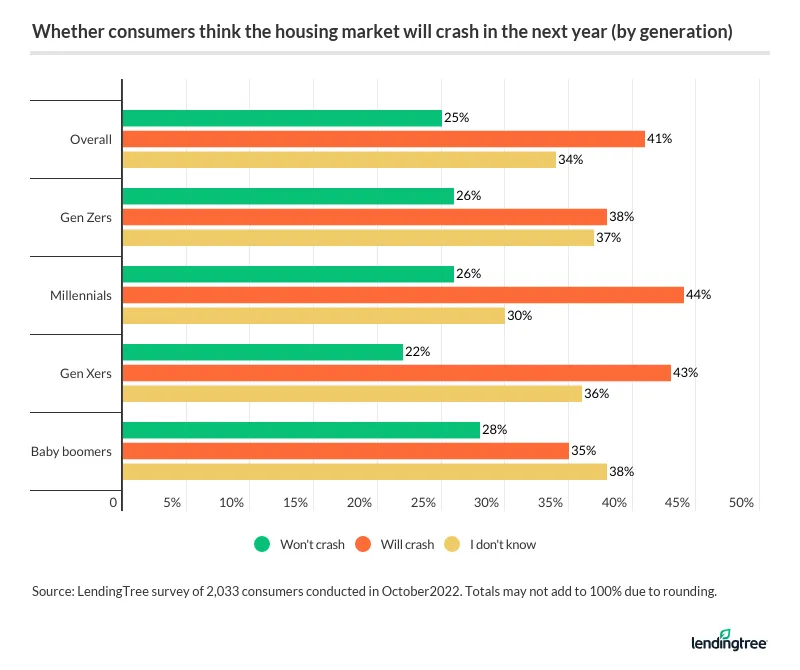

- 41% of Americans believe the housing market will crash in the next 12 months. Millennials are the most likely generation to agree (44%), while baby boomers (35%) are the least likely.

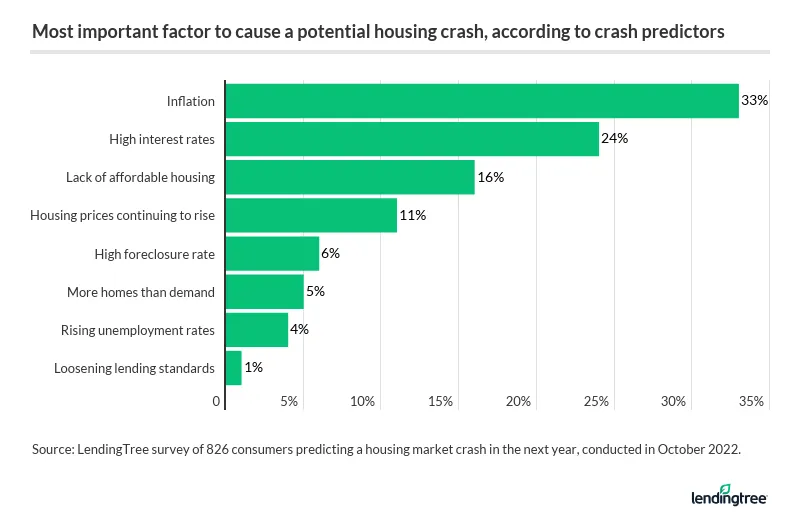

- 74% of Americans who believe the housing market will crash in the next year think it’ll be as bad or worse as the 2008 housing market collapse. Among crash predictors, 33% believe inflation will be the biggest driver, with high interest rates (24%) and a lack of affordable housing (16%) next.

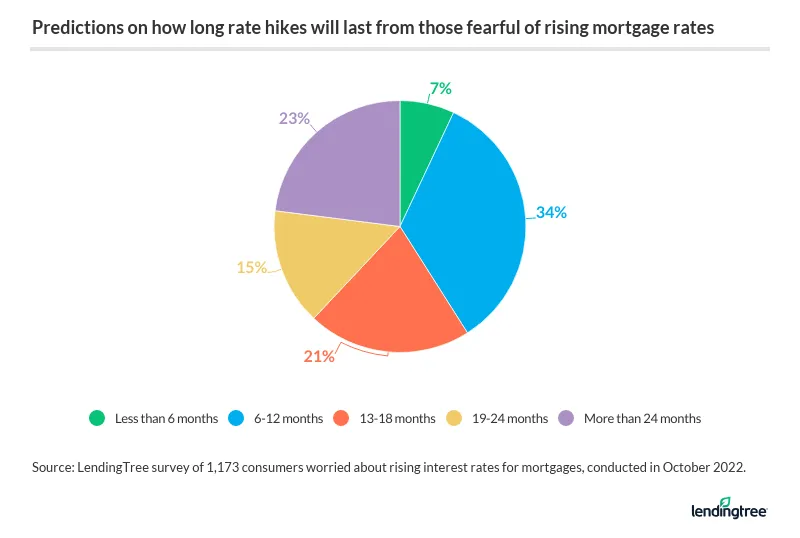

- Regardless of whether the housing market crashes, mortgage concerns weigh heavily on consumers, with rising rates causing worry for 58% of Americans. This is most true among Americans looking to become homeowners (83%) and Gen Zers (68%). Among those concerned about rising mortgage rates, 55% say they’ll rise for another six to 18 months, while 23% think it could be more than two years before rate hikes end.

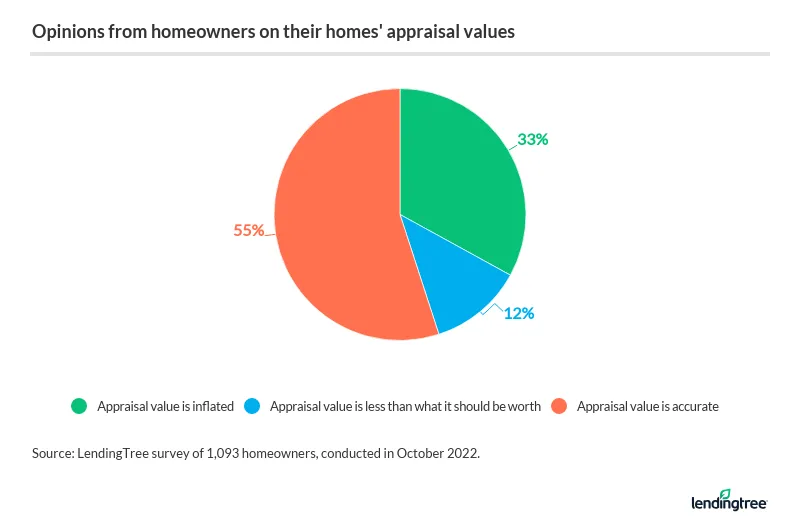

- In uncertain times, an appraisal can provide potential sellers with the estimated value of their home, so it’s helpful that 55% of homeowners think theirs is accurate. Meanwhile, 33% say their estimated home value is inflated, while 12% say the value is less than what they think it’s worth.

- Concerns aren’t just among homeowners, as 61% of renters say the average monthly rent where they live is more expensive than it’s been or what they think it should be. By generation, millennials and baby boomers renters are the most likely to view prices as inflated, with 66% in both groups agreeing.

2 in 5 Americans believe a housing market crash is coming

Consumers are concerned about the economy, and the housing market is no exception. Overall, 41% of Americans believe the housing market will crash in the next 12 months.

By generation, millennials (ages 26 to 41) are the most likely to think the housing market will crash in the next year (44%), though that’s followed closely by Gen Xers (ages 42 to 56) (43%). On the other hand, baby boomers (ages 57 to 76) (35%) are the least likely.

By gender, men (43%) are more likely than women (38%) to think the housing market will crash in the next year.

Crash predictions also vary widely based on education. Specifically, Americans with higher education levels are more likely to say a housing market crash will happen in the next year. To break it down:

- Americans whose highest academic level is a high school diploma: 38%

- Americans who started college but didn’t complete it: 38%

- Americans with an associate degree: 44%

- Americans with a bachelor’s degree: 46%

- Americans with a master’s degree: 45%

It could be worrisome that educated consumers are generally more concerned about a housing market crash, but what do the experts think? According to LendingTree senior economist Jacob Channel, it depends on how you define “crash.”

“While I do think the housing market will continue to slow over the next 12 months and some people may end up underwater on their mortgages as a result, a major crash doesn’t appear likely — at least not at the moment,” he says. “With that said, I do think that home prices will probably come down next year. As of now, 5% to 10% declines in many markets seem reasonable to me.”

Meanwhile, a quarter (25%) of Americans don’t think the housing market will crash in the next year. Their reason? Of this group, 22% say it’s because they don’t think the crash is coming that soon. Instead, they believe the housing market will crash in the next two or three years.

Another 16% say the housing market won’t crash because the supply and demand isn’t there — whether that means there are too few houses for sale or too many buyers. Following that, 15% say the measures being taken to prevent inflation from getting worse will prevent a housing crash and 13% say affordable housing is abundant.

Majority of those who expect a crash think it’ll be as bad (or worse) than 2008

The last major housing market crash weighs heavily on many consumers’ minds, as nearly three-quarters (74%) of Americans who believe the housing market will crash in the next year think it’ll be as bad or worse as the 2008 housing market collapse.

Among crash predictors, 33% believe inflation will be the most important factor driving a housing market crash — making it the most common response. Following that, 24% say high interest rates are the biggest driver, while 16% say it’s a lack of affordable housing.

However, Channel says it’s unlikely the market will crash like it did during the Great Recession — in fact, the very factors that crash predictors worry about can offer some peace of mind.

“Today’s homeowners are in a much better position to continue to make their payments, even if we enter a recession,” Channel says. “It’s important to note that the reason why the market crashed in 2008 was because there was diminished demand for homebuying and a massive influx of homes hitting the market due to high foreclosure rates. Right now, we do have reduced demand for new homes, but no massive influx of supply, which puts us in a much better position.”

Not all crash predictors expect another 2008-style collapse, though — just over a quarter (26%) of those who predict a crash in the next year think it won’t be as bad. And like general crash predictions, this also varies by education level. Among crash predictors, 43% of those with a master’s degree think the housing market will fare better than in 2008. On the other hand, just 1 in 5 crash predictors (20%) whose highest academic level is a high school diploma feel similarly.

Some (particularly crash predictors) are putting off major housing decisions

The current state of the housing market has some postponing major housing decisions. Across all consumers, 48% say they’re postponing major decisions. A third (33%) say they’re either renting or staying in their current home for now and waiting to buy later, while 12% say they’re putting off a renovation or remodeling project.

Crash predictors are particularly likely to put off major housing decisions. Of the group that expects a housing crash in the next year, 58% say they’re postponing housing-related changes, mostly by staying where they currently are and waiting to buy (42%).

Among those who don’t think a housing crash will happen, just 39% are postponing housing-related changes. Over a quarter (26%) of this group say they’re staying where they currently are and waiting to buy.

Rising mortgage rates concern 58% of Americans

A possible crash isn’t the only concern consumers have about the housing market. The majority (58%) of Americans are also worried about rising mortgage rates. According to Channel, these fears are understandable.

“The rate you get on your loan is one of the biggest determining factors for how expensive your mortgage payments will be,” he says. “The higher your rate, the more you’ll end up spending. Rates have risen so dramatically this year that many new would-be buyers are finding themselves priced out of the market.”

Those would-be buyers are most worried about rising rates, at 83%. Following that, the youngest generation is likely worried about being priced out, with 68% of Gen Zers saying they’re concerned.

Meanwhile, just over half (51%) of homeowners are concerned. While Channel says those rising rates wouldn’t impact homeowners with fixed-rate mortgages, those with adjustable-rate mortgages (ARMs) certainly could be affected because their rates adjust based on financial market conditions.

Like crash predictors, those worried about rising mortgage rates have varying predictions about the severity. Of this group, 55% say mortgage rates will rise for another six to 18 months. Another 15% worried about rates believe they’ll grow for another 19 to 24 months, while 23% think it could be more than two years before rate hikes end.

In addition to rising mortgage rates, 3 in 5 Americans (60%) believe housing prices will increase in the next year, while just 26% think prices will decrease. Gen Zers are the most likely generation to expect a housing price increase, at 74%. On the other hand, baby boomers are most likely to expect price decreases, with 37% of this age group expecting lower prices in the coming year.

Majority of homeowners think their appraisal is accurate

A home appraisal, which gives owners an estimate of their home value, can be valuable in an uncertain market. Although consumers are concerned about the housing market, 55% of homeowners think their current home appraisal is accurate. Meanwhile, 33% say their estimated home value is inflated, while 12% say the value is less than what they think it’s worth.

Homeowners with young children (42%), millennial homeowners (42%), Northeastern homeowners (39%) and homeowners making $50,000 to $74,999 (39%) are the most likely to say their estimated appraisal value is currently inflated. Meanwhile, Gen Z homeowners (67%), baby boomer homeowners (62%) and homeowners making less than $35,000 (61%) are among the most likely to say their appraisal value is accurate.

For homeowners concerned about the housing market, Channel says your home appraisal can be particularly helpful.

“Getting your home appraised can provide peace of mind in an uncertain market,” he says. “In some cases, an appraiser can help assuage fears that your home’s value is plummeting. In other cases, they can provide you with more insight into why your home is valued the way that it is and help you understand how you might be able to boost your home’s value.”

Further, he notes that getting an appraisal can also help you see how much you could receive from a home equity loan or something similar. Tapping into a loan could help make your current place feel more livable if you aren’t comfortable buying a new place because of uncertainty about the market or rising rates.

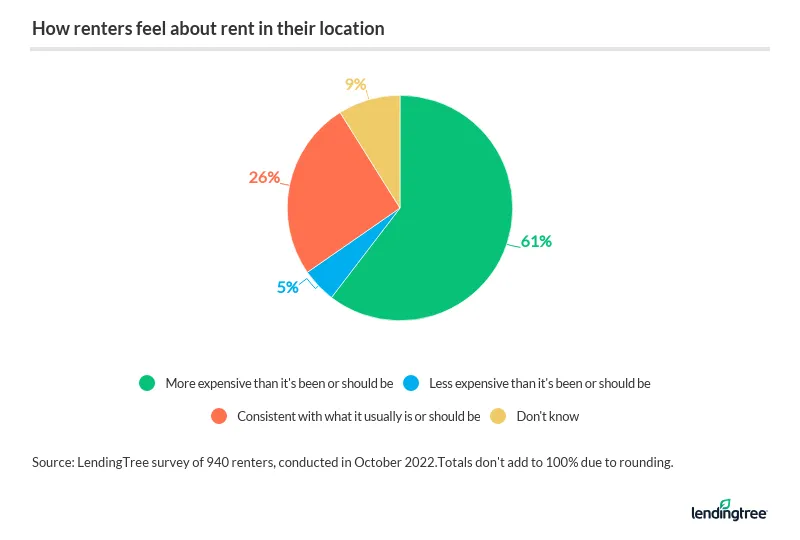

Renters think their rent is too expensive

Concerns extend beyond homeowners. In fact, 61% of renters say the average monthly rent where they live is more expensive than it’s been or what they think it should be. Meanwhile, 26% say their rent is consistent with what it usually is or what they think it should be.

Renters making between $75,000 and $99,999 (77%) are the most likely group to view rent prices as inflated, while six-figure earners (42%) are most likely to view rent prices as consistent. By generation, millennials and baby boomers are the most likely to view rent prices as inflated, at 66% for both. Meanwhile, Gen Zers (35%) are the most likely to think rent prices are consistent.

Expert advice: Staying informed in an uncertain market

Regardless of your predictions, it’s difficult to predict the future of the housing market. However, it’s always best to keep yourself informed.

For some peace of mind, Channel recommends:

- Remember that the value of your home isn’t everything and that your ability to pay your mortgage is generally more important. “If the value of your home does decline and you’re underwater on your mortgage as a result, it’s not the end of the world,” Channel says. “What matters is that you can afford to keep making your current payments. After all, having a safe place to live is ultimately more important than how much your home is worth.”

- If you’re having issues making payments, don’t wait to ask for help. “The sooner you reach out to your lender to tell them that you’re having trouble keeping with your mortgage, the more time you’ll have to work with them and come up with a backup plan,” he says. “From asking for forbearance to selling your current place, the more time you give yourself, the more options you’ll likely have. If you wait until the last minute to ask for help, it could be too late and you could face foreclosure.”

- Don’t panic. “Over the long term, housing is generally a very stable asset,” Channel says. “A temporary decline in prices doesn’t necessarily mean that you’ll always be behind on your mortgage or unable to sell your house for a profit. By panicking and selling prematurely, you could end up losing money. Keep in mind that even though the housing market collapsed during the Great Recession, they eventually rebounded. Even if prices fall over the next year or two, odds are that they’ll rebound sooner rather than later.”

Methodology

LendingTree commissioned Qualtrics to conduct an online survey of 2,033 U.S. consumers ages 18 to 76 on Oct. 18, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

- Generation Z: 18 to 25

- Millennial: 26 to 41

- Generation X: 42 to 56

- Baby boomer: 57 to 76

View mortgage loan offers from up to 5 lenders in minutes