62% of Renters Worry They’ll Never Own a Home

Homeownership has long been viewed as a cornerstone of the American dream, but it’s never been achievable for everyone. This can feel especially true in today’s housing market, where relatively steep (albeit gradually declining) mortgage rates and high home prices have made homeownership too expensive for many would-be buyers.

In fact, today’s market appears so unfriendly that a majority of renters fear the dream of homeownership is out of reach. More specifically, according to LendingTree’s latest survey, 62% of renters say they’re worried they’ll never be able to own a home.

Read on to learn more about how Americans view homeownership and get a sense of why owning is preferable for some and less desirable for others.

Key findings

- Nearly 2 in 3 renters fear they’ll sign leases forever. 62% of renters worry they’ll never be able to own a home. Although 93% of Americans think homeownership is part of the American dream, 36% say it’s less so than it used to be.

- Most Americans prefer being a homeowner. 83% of Americans would rather own a home than rent. Among those who would rather own, the flexibility to do what they want with the space is the No. 1 reason (62%), followed by stability (61%), no rules against pets (49%) and pride in homeownership (48%).

- That said, renting is good enough for the rest. 17% of respondents say they’d rather rent than own in an ideal world. Among this group, 51% say it’s because they don’t want to be responsible for maintenance or repair costs, while 44% say it’s more affordable and 37% say they don’t want to be responsible for property taxes.

- For those who rent but would prefer to own, cost is the biggest barrier. 65% of this group say the cost of a down payment is holding them back from purchasing. Additionally, 52% say home prices are too high in their areas and 39% say their credit score makes it hard to qualify for a mortgage.

- Whether you rent or own, there are drawbacks. While owning a home is the dream for most Americans, 34% of homeowners most dislike the cost of maintenance or repairs, while 33% cite property taxes. Among renters, the top dislikes are unexpected rent increases (30%) and landlords (21%).

For many, homeownership is part of seemingly unreachable American dream

Despite plenty of homebuying hurdles, 93% of Americans think homeownership is part of the American dream. This belief is widespread across Americans regardless of gender, age, parental status or household income.

For example, women (94%) and men (93%) nearly equally say homeownership is part of the American dream. There’s also consensus among different generations, old and young. In fact, 97% of baby boomers (ages 60 to 78), 96% of Gen Xers (ages 44 to 59), 92% of Gen Zers (ages 18 to 27) and 90% of millennials (ages 28 to 43) say the American dream involves homeownership.

Parents are generally more likely to associate homeownership with the American dream than nonparents, but not by much. In fact, 97% of parents with children 18 or older and 95% of those with kids younger than 18 say owning a home is part of the American dream. That figure is 90% for adults without kids.

In the same way not having a child can change perceptions, earning a lower income can make some less likely to associate homeownership with the American dream. In fact, 90% of those in households earning less than $30,000 a year say owning a home is part of the American dream. That’s a bit lower (but still comparable) to the 96% who earn at least $100,000 a year and say the same.

Though associating the American dream with owning a home is widespread, 62% of renters worry they’ll never be able to own. Some are more worried than others. For instance, 66% of female renters say they worry they’ll never own, compared with 57% of male renters. Millennial (67%) and Gen Z (66%) renters are more afraid than Gen X (60%) or baby boomer (49%) renters.

Commonly cited obstacles to homeownership include an inability to afford a down payment (cited by 65% of renters who would prefer to own), prohibitively high home prices (52%) and a lackluster credit score (39%).

While the housing market isn’t likely to become much more affordable as 2024 comes to an end, it’s still likely to become somewhat cheaper. As mortgage rates continue to decline, buying may appear less out of reach to some renters than a month or two ago.

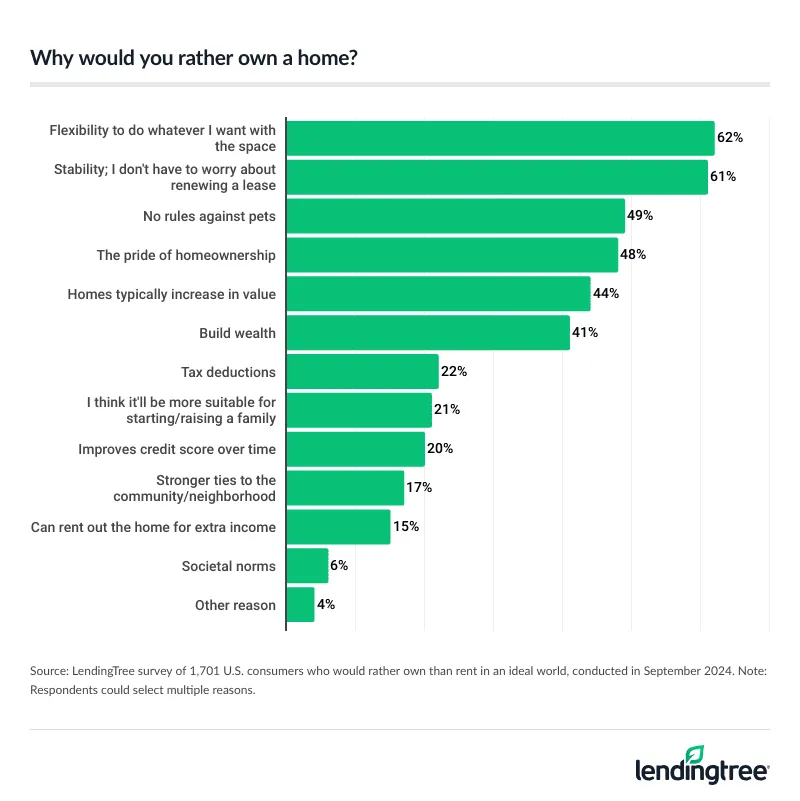

Flexibility, stability are key reasons why most Americans would rather own

Becoming a homeowner is often easier said than done, but 83% of Americans say they’d rather own a home than rent one in an ideal world.

Across all demographics surveyed, no fewer than two-thirds say they prefer owning over renting. Even in demographics where homeownership is less prized, like those earning less than $30,000 a year, those without children and Gen Zers, a significant majority (76%, 77% and 79%, respectively) still say they’d rather own than rent.

Overall, 62% of those who say they’d rather own listed the flexibility to do whatever they want with the space. Similarly, 61% cite stability, namely not needing to worry about renewing a lease. Outside of flexibility and stability, freedom to have pets (49%) and pride in homeownership (48%) are the next most commonly listed.

Notably, the potential long-term monetary gains of homeownership seem less important to those who’d rather own than flexibility, stability and even pride. Only 44% of those who say they’d rather own included home price appreciation among the reasons behind their preference, while 41% listed wealth-building.

While wealth-building is an important part of owning a home, it isn’t the end-all, be-all. On the contrary, the potential for more freedom and stability can provide plenty of justification for those looking to become or remain homeowners.

Of course, would-be buyers should still remember that freedom has a price. Having more say over your space isn’t always worth higher bills, especially if you can’t afford to buy a house without stretching your budget beyond its breaking point.

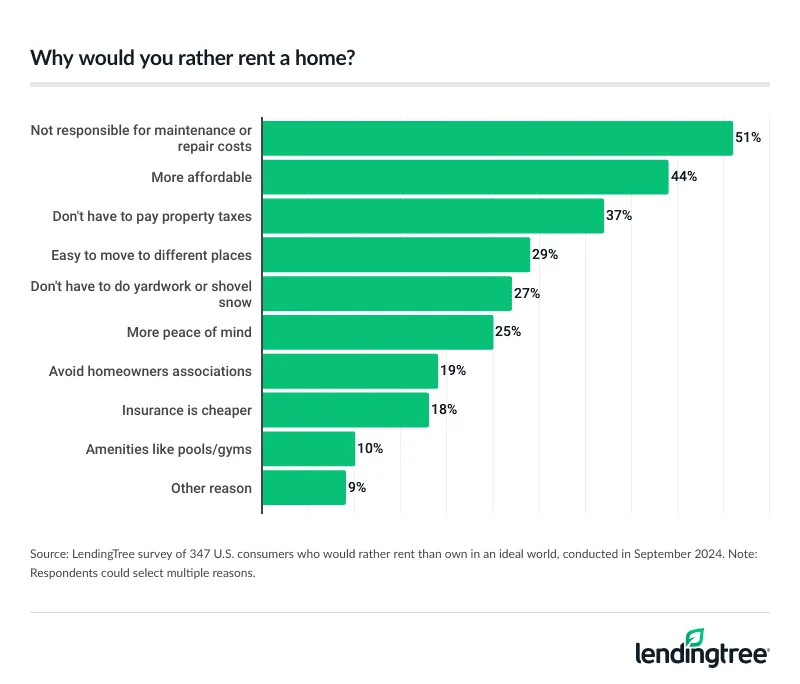

While most would rather be homeowners, renting still has perks

Of those surveyed, only 17% say they’d rather be renters than homeowners. Among current renters, that figure jumps to 34%, but it still pales in comparison to the 66% of current renters and 97% of current homeowners who say they’d rather own.

Even so, renting has some perceived benefits over homeownership — chief among them is lower costs. For example, 51% of those who say they’d rather rent cite not being responsible for maintenance or repair expenses. Meanwhile, 44% prefer renting because it’s generally more affordable, and 37% cite not needing to pay property taxes.

There are also positives associated with renting outside of its cheaper price point. In fact, 29% of those who prefer renting list more freedom to move as a reason, and 25% went so far as to say they feel renting is preferable to owning because it provides them more peace of mind.

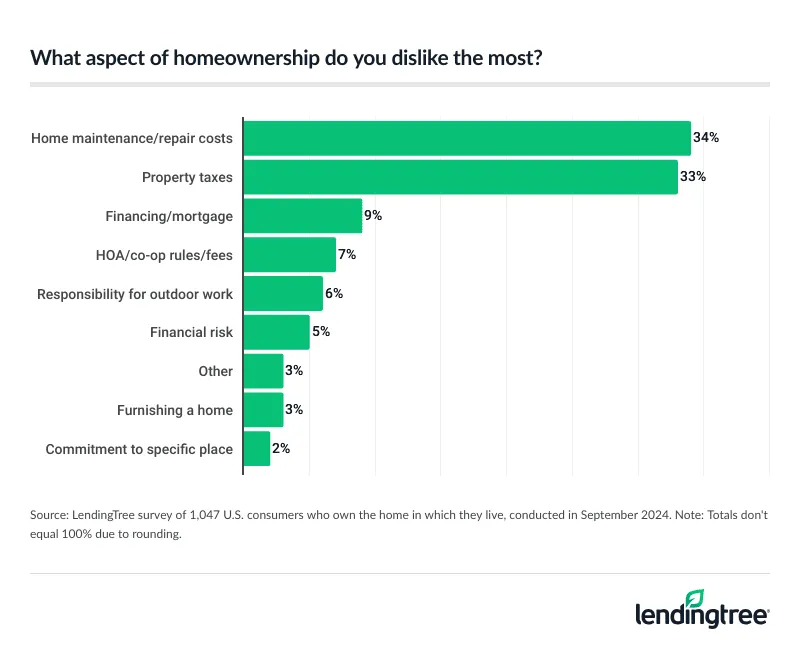

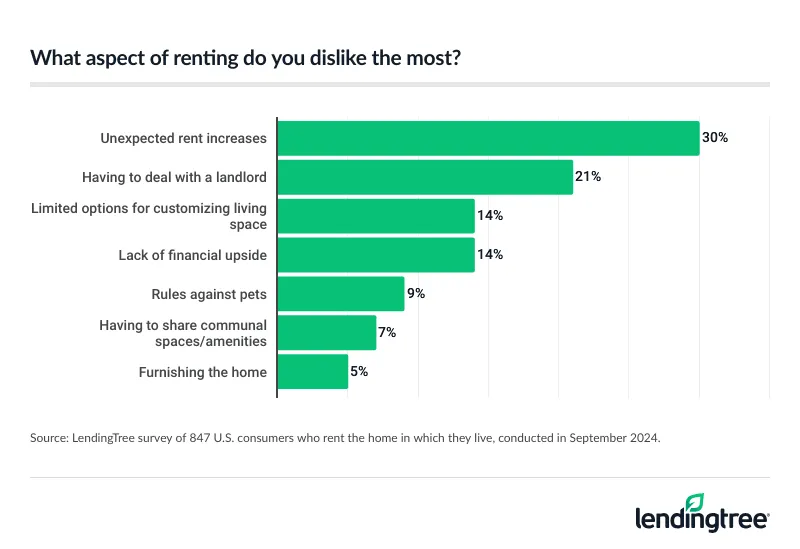

Whether you own or rent, there are bound to be drawbacks

Regardless of your preference, neither renting nor owning is likely to be sunshine and rainbows. In fact, there are plenty of things homeowners and renters dislike about their living situations.

For homeowners, 34% say dealing with home maintenance and repair costs is their least favorite part of owning a house. Meanwhile, 33% say it’s having to pay property taxes.

As far as renters are concerned, unanticipated rent hikes are the most disliked thing about renting, at 30%. Next, 21% say needing to deal with a landlord is their biggest gripe.

Of course, while there are drawbacks to renting and owning, it’s worth pointing out that homeowners tend to be happier with their living arrangements than renters. In fact, 82% of those who currently own their home report being satisfied with their housing arrangements. That’s considerably higher than the 53% of renters who say they feel the same way.

3 tips for those looking to transition from renting to owning

If you’re ready to take the leap from renting a home to buying one, the following tips can help you get prepared and save money.

- Know what you’re getting yourself into. As mentioned, homeownership isn’t always a walk in the park, and neither is homebuying. It can take weeks or even months to get approved for a mortgage, find a house you want, make an offer, get it accepted and move in. On top of that, once you own a home, you’re responsible for upkeep and property taxes. The grass can sometimes appear greener on the opposite side of the fence. There’s no shame in remaining a renter if you realize you can’t afford to buy a house, or if you’ve decided you don’t want the responsibilities of homeownership.

- Start strengthening your finances right away. The more time you give yourself to create a budget, save for a down payment and pay down other debts, the stronger your finances are likely to be by the time you apply for a loan. You don’t need to be perfect to get approved for a mortgage, but the less debt you have, the stronger your credit score is, and the more cash you have for a down payment, the higher your odds of approval. Having strong finances and at least 20% for a down payment can help you snag more favorable loan terms or avoid paying extra costs like private mortgage insurance (PMI).

- Shop around for a mortgage. Though sometimes overlooked, shopping around and comparing offers from different lenders is an important part of homebuying. Different lenders can offer different rates to the same borrowers. By shopping around before you get a mortgage, you could increase your chances of snagging a lower rate and, in turn, lowering your monthly payments and making homebuying more affordable.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,048 U.S. consumers ages 18 to 78 from Sept. 13 to 17, 2024. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2024:

- Generation Z: 18 to 27

- Millennial: 28 to 43

- Generation X: 44 to 59

- Baby boomer: 60 to 78

View mortgage loan offers from up to 5 lenders in minutes