77% of Americans Say the Housing Market Is ‘Prohibitively Expensive,’ Though 21% Still Consider Buying This Summer

Despite signs that the housing market is becoming (slightly) friendlier to would-be buyers, home prices and mortgage rates remain steep. This has led to mortgage demand hovering around its lowest level in over 20 years.

Demand probably won’t spike anytime soon because, according to the newest LendingTree survey, 77% of Americans say the housing market is “prohibitively expensive.” While 21% are still considering a home purchase this summer, our findings highlight how daunting today’s market appears to most people.

Read on to learn more about how Americans feel about the market, and how — despite trepidations — some remain hopeful about their ability to purchase a home.

Key findings

- Buying a home isn’t in the forecast for most Americans this summer. While 77% of Americans believe the housing market is prohibitively expensive in their area, 21% are still considering buying a home this summer. Gen Zers are most likely to be on the hunt for a new home this summer, with 37% considering buying.

- Some potential buyers are optimistic. Among those considering buying this summer, 56% are confident they’ll be able to find and close on an affordable house that fits their needs, and 44% are buying because they believe they’ll get a good deal. However, 19% don’t think a deal is possible because mortgage rates are too high.

- Few think rates or home prices will improve anytime soon. 86% of respondents think mortgage interest rates will rise or stay the same this summer; among them, 23% worry rates will never fall. Additionally, 87% believe home prices in their area will rise or stay the same this summer; among them, 36% think high home prices are here to stay.

- Economic concerns weigh on potential homebuyers this summer. Among summertime home shoppers, their top concerns about buying now are high home prices (35%), high mortgage interest rates (27%) and finding the right house (18%). Interest rates are top of mind for current mortgage holders, as 29% feel trapped in their homes due to their current rates.

For most, homebuying not in the cards this summer

Though the housing market tends to become more active as the weather heats up, this summer’s market isn’t poised to be particularly hot. With 77% of Americans saying the homes in their area are too expensive — led by 81% of Gen Xers ages 44 to 59, women and parents of young kids — most would-be buyers are likely to remain on the sidelines until the market becomes more affordable.

That said, some are still considering buying in the next few months, with certain demographics more gung ho than others.

Gen Zers ages 18 to 27 (37%) are most likely to consider buying a home this summer, ahead of 36% of parents with kids younger than 18. Overall, 21% of Americans are thinking about it.

As for why, reasons vary. For example, Gen Zers are less likely to be current homeowners than members of older generations. As a result, some may feel more inclined to navigate today’s expensive market if they can transition out of another living situation like renting or crashing with Mom and Dad.

Families with young kids might see moving before summer ends and school starts as more of a necessity than those who don’t need to worry about uprooting little ones during the school year.

Would-be summer buyers generally confident they’ll find a home

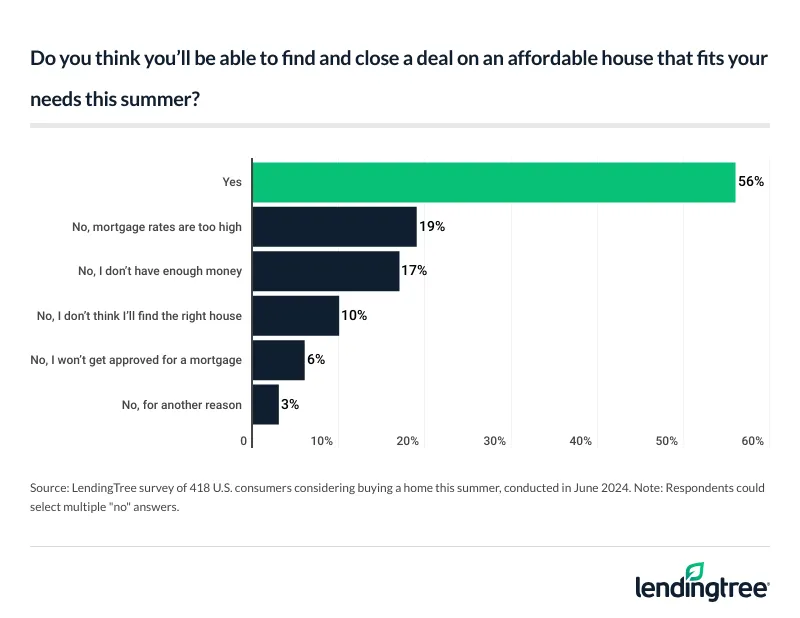

Of those considering buying a house this summer, 56% say they think they’ll be able to find and close a deal on a home that’s affordable and fits their needs. (Generationally, this is highest among millennials ages 28 to 43 at 59%.)

As for those who say no, reasons range from high mortgage rates to approval concerns.

When asked why they were thinking about moving, 44% of potential buyers said they believed they would be able to find a good deal on a house. Another 37% say they’ve outgrown their current home, while 10% are headed to a new town, city, state or country.

Despite some optimism, buyers and sellers have plenty of concerns

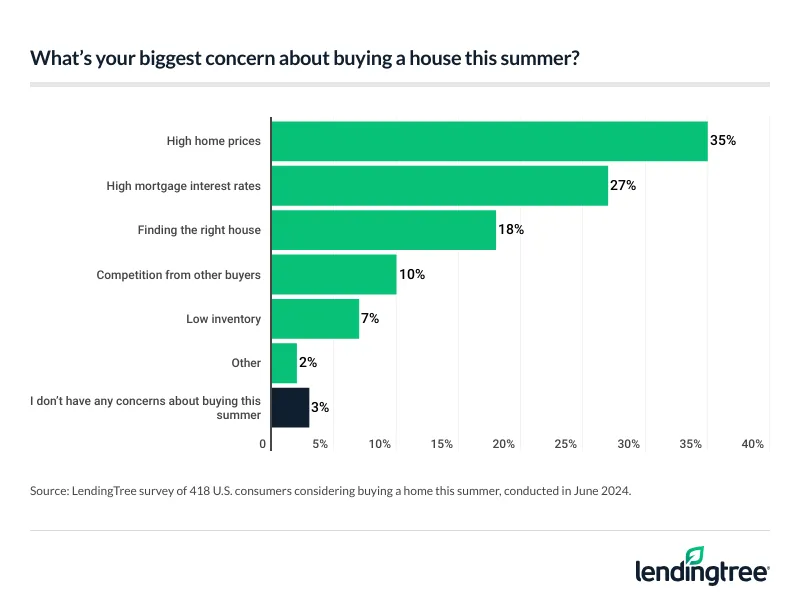

Just more than 1 in 3 (35%) considering buying a house this summer cite high home prices as their main worry. Similarly, 27% say high mortgage rates. Finding the right home (18%), competition from buyers (10%) and low inventory (7%) are also common worries.

Like buyers, possible summertime sellers also have concerns. Four in 10 (40%) say their biggest worry about selling this summer is receiving a fair offer. Another 26% are afraid they may not be able to find another home, while 23% worry there isn’t enough buyer demand.

In truth, all these apprehensions are valid. Buyers and sellers alike can run into plenty of headwinds in today’s market, and buying and selling are often easier said than done.

But legitimate concerns don’t make all worries insurmountable. Homes are still being bought and sold across the country. With patience and a willingness to compromise, buyers and sellers can increase their odds of getting what they want from today’s market.

Remember, having concerns is OK, especially if you’re considering engaging in a transaction worth six or more figures. However, you shouldn’t let yourself become so consumed by worry that you fail to act on good deals that may present themselves.

High rates can make buying unappealing for current homeowners

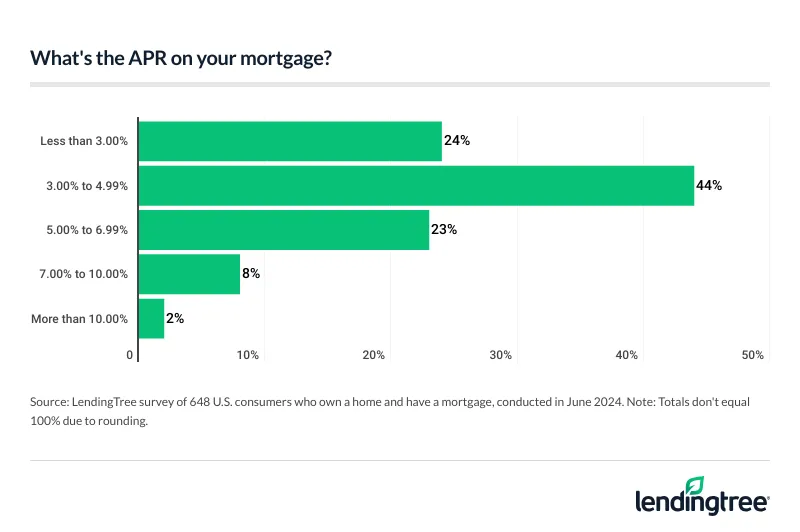

It’s easy to blame high home prices for why today’s housing market is so unattractive to buyers, but mortgage rates also play a major role. This can be especially true for current homeowners, 67% of whom have an APR below 5.00%. For comparison, the average rate on a 30-year, fixed-rate mortgage was 6.95% when this survey was fielded.

Given how much lower their rates might be than those offered on new loans, it’s understandable why 29% of homeowners with a mortgage feel “trapped” in their house by their current mortgage rate. This is highest among parents with young kids (38%), millennials (34%) and men (33%).

Even if they don’t feel like they’re entirely out of options when it comes to selling and buying a new place, parting ways with a sub-5.00% mortgage rate is likely going to be a tough pill for most homeowners to swallow.

Rates are high, but will they go even higher? Many say yes

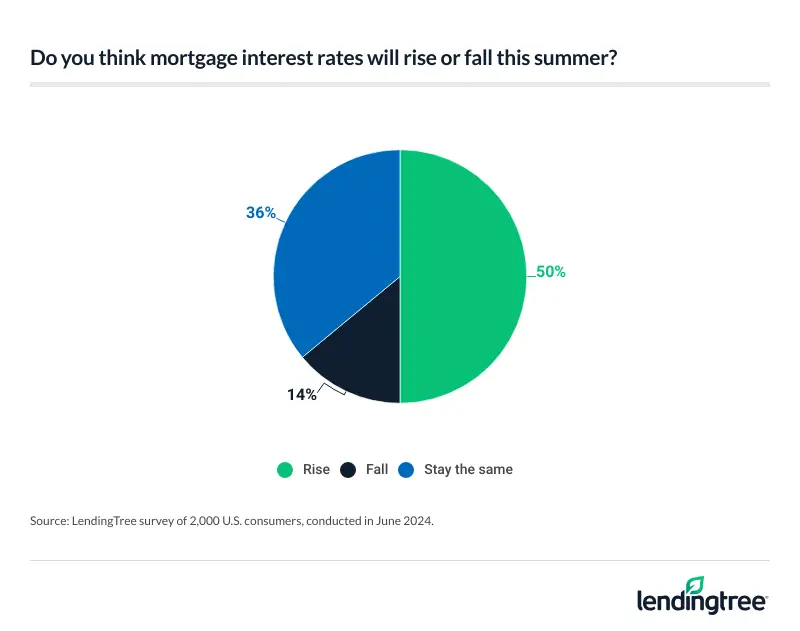

Half (50%) of Americans believe mortgage rates will rise over the remainder of this summer. Another 36% are a bit more positive, thinking they’ll stay the same, while 14% are optimistic they’ll fall. On average, respondents think mortgage rates will average 9.53% by next June.

When our survey was fielded on June 13 and 14, the average interest rate on a 30-year, fixed-rate mortgage was 6.95%, according to Freddie Mac. At the median level, respondents thought the average rate was 7% — right on the money. On average, though, respondents thought the average rate was nearly three percentage points higher at 9.87%.

Being off by three percentage points might not seem like a huge deal, but the difference is nothing to scoff at. For instance, the monthly payment on a $350,000 30-year, fixed mortgage with a 6.95% interest rate is about $2,317 (excluding additional costs like taxes and insurance). That same loan would cost $3,038 a month — or $721 more — with a 9.87% rate.

Ultimately, it’s impossible to say where mortgage rates will land over the coming months and years. But some silver linings are beginning to emerge. For example, if inflation continues to cool and the Federal Reserve starts cutting its benchmark rate in September, mortgage rates may end the year closer to 6.00% than 7.00%.

3 tips for summer house hunters

There’s no sugarcoating how expensive and hard to navigate today’s housing market can be. The following tips can help make buying this summer an achievable goal:

- Shop around for a mortgage. As mentioned, the rate you get on a mortgage greatly impacts your monthly payments. Because different lenders can offer different rates to the same borrowers, shopping around and comparing multiple mortgage offers from different lenders can help you secure a lower rate than the first lender offers. This lower rate can not only reduce your monthly mortgage payments and make buying more affordable, but it can also reduce the amount of money you spend in interest over your loan’s lifetime by tens, if not hundreds, of thousands of dollars.

- Budget carefully. Before thinking about buying, sit down and evaluate how much you can afford. A monthly mortgage payment isn’t the only thing you need to worry about when crafting a budget. Upfront costs such as a down payment and moving fees can quickly add up, as can expenses like repairs. If you rush to buy without evaluating what you can afford, you risk biting off more than you can chew and becoming house poor.

- Negotiate. Sellers generally appear more willing to negotiate on things like price than last year or during the height of the pandemic. While you may not get a massive discount, having an open and respectful conversation with a seller could help you get a better deal. Even if a seller is unwilling to offer you a lower price, they may be willing to offer other concessions, like paying for closing costs or upgrading outdated appliances.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,000 U.S. consumers ages 18 to 78 from June 13 to 14, 2024. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2024:

- Generation Z: 18 to 27

- Millennial: 28 to 43

- Generation X: 44 to 59

- Baby boomer: 60 to 78

View mortgage loan offers from up to 5 lenders in minutes